Budgeting Basics

Budgets are like the New Year’s resolutions of personal finance. We all know we should have one and we all know it’s a fairly simple thing to follow—at least in theory. Like resolutions, we often map out personal budgets with the best of intentions, only to abandon them a couple of weeks later.

It’s easy to blame our budget failures on the numbers we use, or the categories we create, or even the specific app or budgeting system we choose—but more often than not, the underlying cause of a hard-to-stick-to budget is our relationship with it. Just like resolutions, if we design budgets that are too restrictive or too vague, there’s no motivation to follow them.

Whether you’re planning your first budget or re-evaluating your current budget, the ground rules listed below will set you up for success by changing the way you look at budgeting. It doesn’t matter if you manage your budget on your smartphone or if you prefer good ol’ pen and paper—these budgeting basics can be applied to every budgeting system.

Budgeting Basic #1: Budgeting is about confidence, not guilt

A reason lots of people avoid budgeting is because they think it means giving up everything they love and converting to a super-frugal lifestyle. Or they might be scared they’ll discover that they’ve been spending lots of money on the “wrong” things.

Budgeting is not meant to shame you into being financially responsible. At the end of the day, budgeting is simply about awareness. If you fully understand where your money is going each month, you can design a budget that allows you to truly enjoy your money. How fun is a shopping spree if it’s what’s keeping you in credit card debt for another month? How much can you enjoy your new apartment if the rent payment is stressing you out? Budgets are helpful when it comes to managing your bills and saving up for future expenses, but they’re also the key to spending your money confidently.

Budgeting Basic #2: Stop comparing yourself to others

An effective budget is tailored to your specific combination of wants and needs, so forcing yourself to live within a sample budget you found online or in a personal finance book is not a long-term solution. Budgeting categories can vary wildly depending on where you live, where you work, how you get from point A to point B, what you do for fun and what your personal goals are. Finding a budget that works for you will take trial and error, and the end result will look different from every other budget out there. Get comfortable with the idea that everyone has different priorities, and that no two budgets look alike.

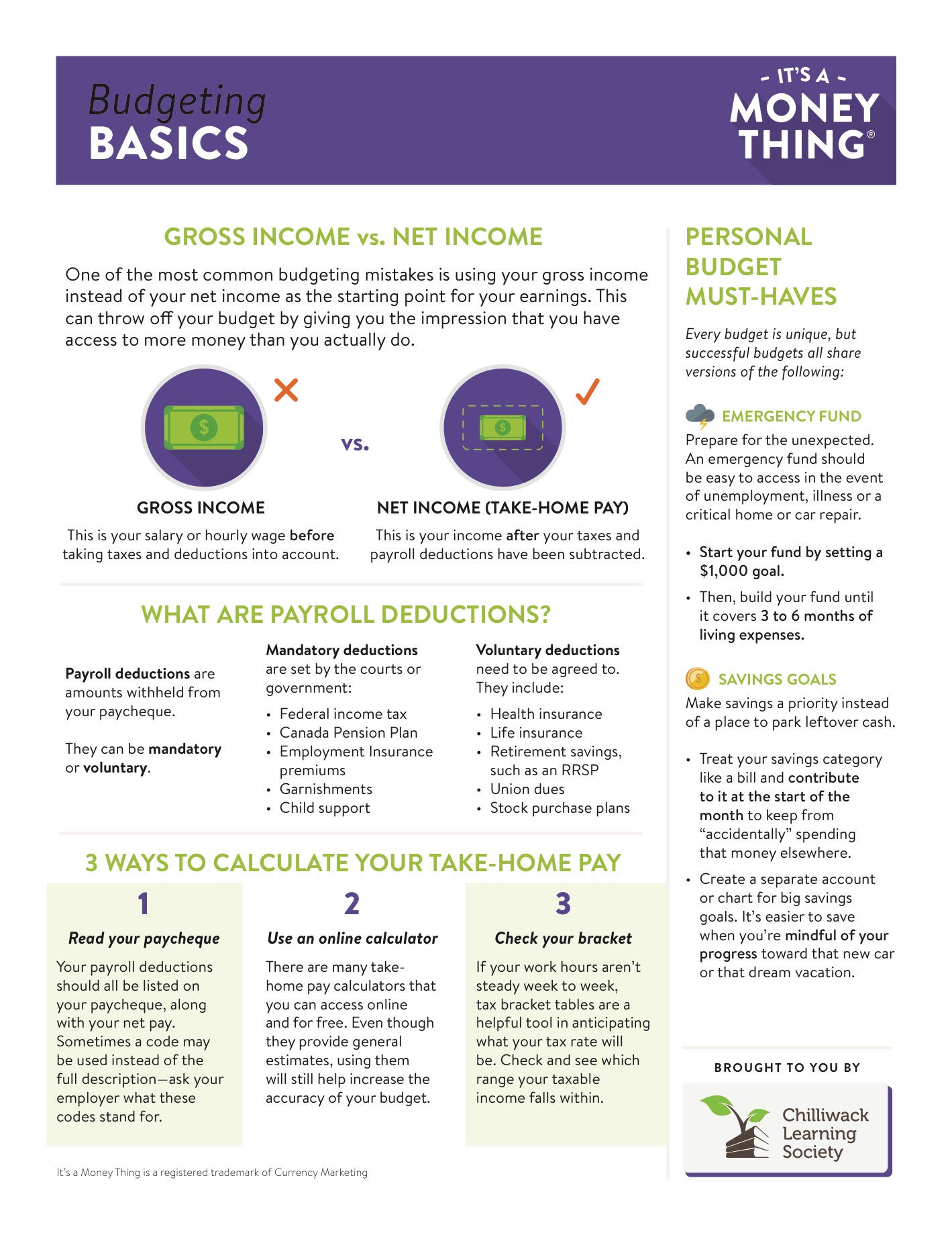

Budgeting Basic #3: Be real about your income

A rookie mistake when it comes to budgeting is using your salary (divided by 12 months) or your hourly wage (multiplied by hours worked) as your monthly income. Instead, take a couple of minutes to calculate your monthly take-home pay—this is your income after estimated taxes and other deductions (like health care, employment insurance premiums and retirement savings contributions) have been taken into account. Your deductions should be listed on your paycheque, and there are plenty of income tax estimate services online that you can use for free.

Budgeting Basic #4: Savings is an expense, too

If budgeting categories were a high school gym class, savings would be picked last. In many budgets, the savings category ends up getting whatever is left over after the “more urgent” expenses have been paid (and—in most cases—the not-so-urgent ones too!). The only way to take your savings seriously is to give it the same priority as your living expenses. If you contribute a set amount to your savings at the beginning of the month, your savings will grow so much faster and you won’t be able to “accidentally” spend that money on something else.

Budgeting Basic #5: Look to your budget instead of your balance

For many people, budgeting simply means checking your account balance before making a purchase—and although it’s good to stay on top of your account totals, looking at your balance is an unreliable way of determining what you can and can’t afford. Your account balance can’t communicate, for instance, how much money needs to be left untouched in order for you to pay your taxes this year or to renew your gym membership next month or to repair your car next week. Get into the habit of referencing your budget instead of your account balance before spending your money.

Budgeting Basic #6: Prepare for emergencies

Emergency expenses have a knack for breaking even the best budgets because they can very easily turn into a huge source of debt. If you don’t have the cash on hand to take care of them immediately, you’ll have to put them on a card or take out a loan, which will have you paying interest on top of the cost of the expenses.

Emergency funds are an important part of any budget and should be a separate category from general savings goals. In order to be effective, your emergency fund can only be accessed for real emergencies—like sudden unemployment, an unexpected medical emergency, or a critical home or vehicle repair. Instead of looking at your emergency fund like yet another savings category, look at it as a way to strengthen your entire budget. Not only will it cover tough situations, but it will also save you stress and give you peace of mind.

Loading...

Loading...

Downloads

-

Loading...

-

Loading...

-

Loading...

-

Loading...