Investment Strategies For These Low-Interest Times

Everyone has some idea of what it means to be money smart—however, whether or not you’ve acted on that idea is a different story! There are a few nuggets of financial wisdom in particular that are echoed so many times in articles, blog posts and TV segments that they become clichés, albeit practical ones. Curb your spending. Pay off your debt. Contribute to your savings early and often. Compound interest is your friend. Start saving now and watch your money grow.

Being financially responsible starts with putting some of those clichés into action, but in doing some research into savings strategies, you might be in for an unpleasant surprise. You might do some quick calculations with current interest rates and come to the sobering realization that the effects of saving your money aren’t as mind-blowing as you thought. Why is that?

The economic landscape has changed a lot in the past 20 years. Our parents saw a time where it was possible to put your money away in a term deposit with interest rates upwards of 10%. Strategically utilizing investments with that kind of return was a smart move and a great way to grow your money over time.

Unfortunately, those days of 10% interest rates seem to have disappeared along with the era of acid-wash jeans and Troll dolls. Current interest rates are at historic lows, and the Bank of Canada predicts that the trend is going to stick around for a while. Saving is, of course, still a crucial part of your financial well-being, but what’s the best way to grow your money and beat inflation when interest rates are near 0%? Consider the following strategies:

CHECK YOUR EXPECTATIONS

What’s the deal? There’s no way to sugarcoat it; interest rates are low right now. As a result, your investments—even with the mighty power of compound interest—just aren’t going to perform as well as they would have in the past. Countering the effects of inflation is another resulting challenge. For millennials, the dream of someday being able to live solely off of the interest generated by investments is suddenly a very tall order. But don’t get too discouraged—as a young investor, time is on your side. Even low-yield investment products can generate significant wealth over long periods of time (we’re talking decades), but it’s important to stay realistic with your long-term savings goals. Will your investment allow you to buy your own island when you retire? It’s highly doubtful, but with some foresight and planning, your investment can allow you to retire comfortably and with peace of mind.

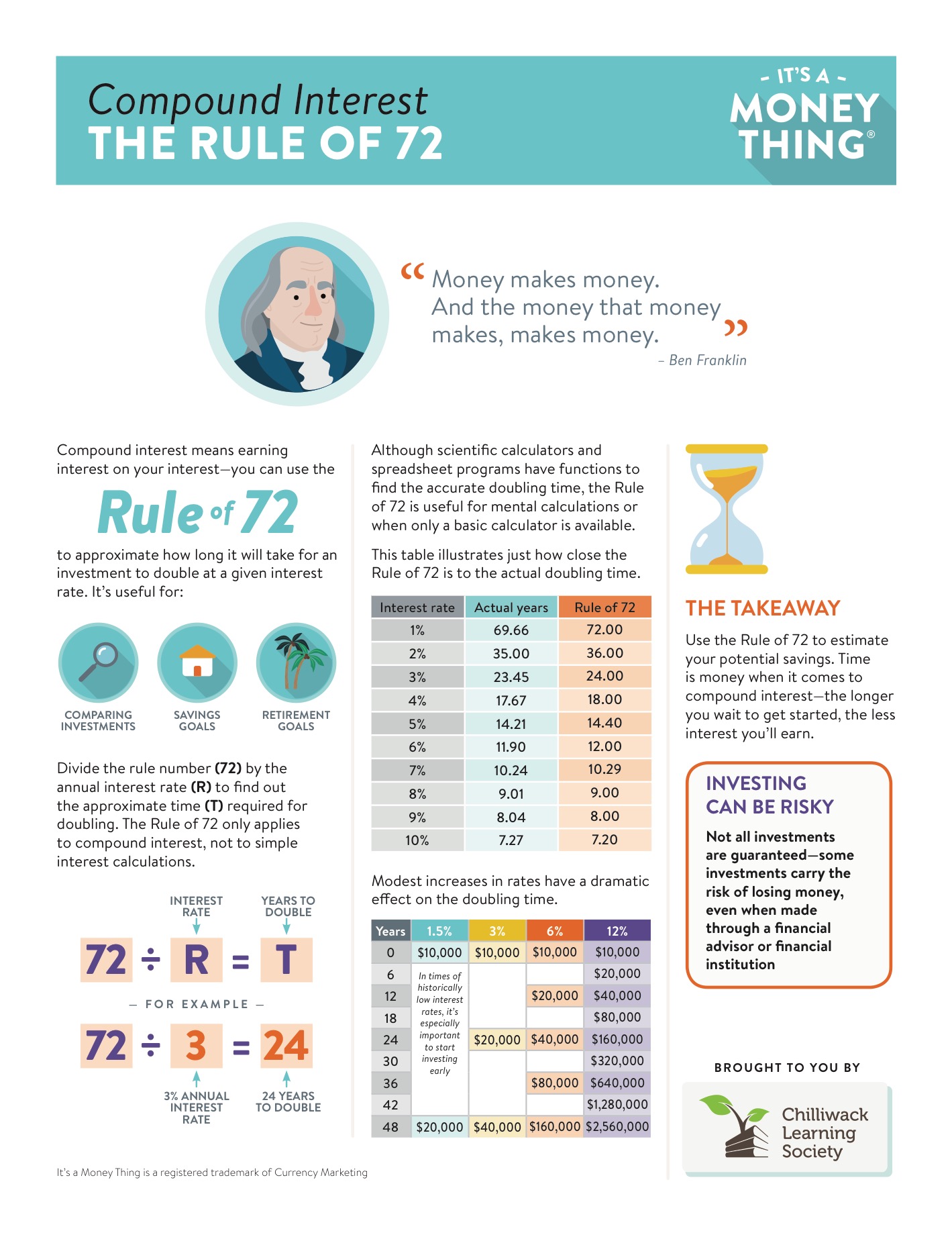

What can you do about it? If you want to be realistic about your investment earnings and help plan for your future, the Rule of 72 is a handy tool to quickly estimate how many years it will take to double your investment at a given rate. The Rule of 72 works with investments that have compounding interest. You simply divide 72 by the rate of annual return (that’s your interest rate). What results is an approximation of how many years it will take for you to double your investment. For example, if you park $1,000 in a term deposit yielding 2% interest, it will take 36 years to double (72/2=36). The Rule of 72 allows you to do some quick, back-of-the-envelope math when comparing different investment options or when planning out your long-term financial goals.

LOVE THE LONG TERM

What’s the deal? As mentioned above, even when interest rates are low and the forecast is bleak, time is still on your side. That’s because the longer your investments have to mature, the more time they have to recover from periods of economic depression. Your long-term money is less susceptible to day-to-day (or even year-to-year) market changes than shorter-term investments.

What can you do about it? Time is compound interest’s best friend. Consider looking into investment products—such as dividend-paying stocks—that contribute to the effects of compound interest. In this investment vehicle, companies share a percentage of their earnings between their shareholders (in the form of cash or additional shares), which can then be reinvested. Throw a long-term investment period into the mix and you have a recipe for some compound interest benefits. Keep in mind that, as with any investment vehicle, nothing is guaranteed and you are always taking on an element of risk.

PUT MANY EGGS IN MANY BASKETS

What’s the deal? There is always an element of risk present in any investment situation. Putting all your eggs in one basket (in this case, putting all your investment dollars behind a single company or a single form of investing) makes you more vulnerable to changes in the economy. Some industries are hit harder by market changes than others. Also, market changes affect investment products differently (for example, bond prices move in the opposite direction of interest rates). Diversifying your investment portfolio is a sound way to minimize (though not completely eliminate) your investment risk.

What can you do about it? By investing in a variety of industries using a variety of assets (stocks, bonds, commodities) your investment dollars are generally less vulnerable to any one sudden change. Consider mutual funds as an investment option. Mutual funds are professionally managed investments that pool together several investors’ contributions and spread them out over various stocks, bonds and securities across several industries. As with every form of investment, mutual funds present their own set of pros and cons; they also carry a degree of risk.

SET UP A SAFETY NET

What’s the deal? At the end of the day, interest rates—just like the economy itself—are unpredictable. Planning ahead is smart, but no amount of researching and strategizing will give you complete immunity from the twists and turns of market forces.

What can you do about it? Beef up your emergency fund. Should a sudden economic change put you in financial hardship, you’ll have three to six months’ worth of expenses as a cushion to figure out a game plan. An emergency fund sitting in your bank account may not earn you as much interest as it would if that money was invested instead, but the point of the fund is that it’s available and quickly accessible in times of need.

________________

While interest rates may be low, you do have options. Start early, invest wisely and give yourself the time you need to reach your goals. And remember, you aren’t alone. Seek advice from a financial planner or stop by your friendly neighbourhood credit union branch to sit down and talk with a professional about your options.

Loading...

Loading...

Downloads

-

Loading...

-

Loading...

-

Loading...

-

Loading...