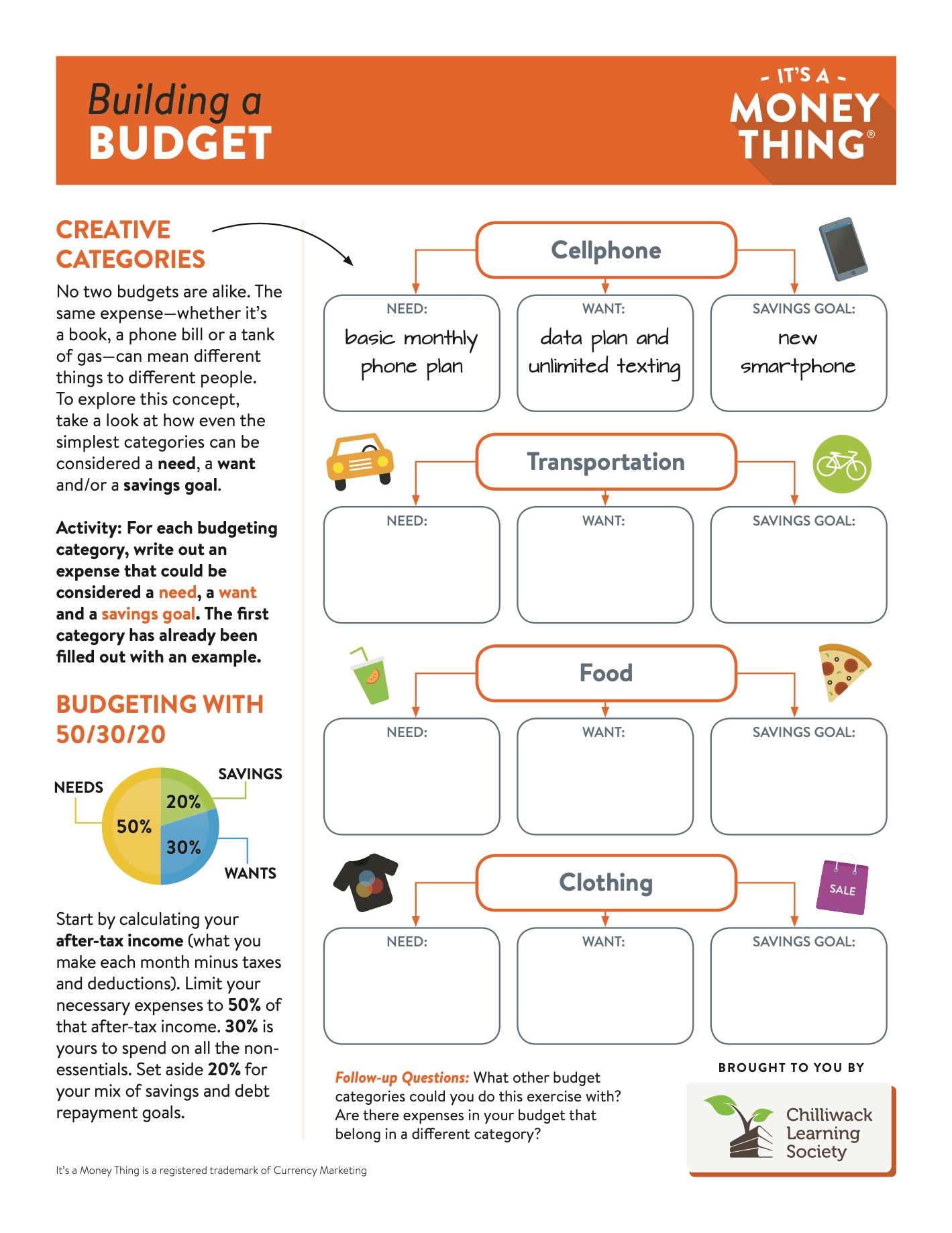

Budgeting with 50/30/20

Budgeting is a skill that helps you make smart decisions with your money. It ensures that you’re spending less than you earn, it prepares you for life’s curveballs, and it funds your goals and your dreams. Unfortunately, budgeting is often seen as restrictive and overwhelming. Financial priorities are deeply personal, so it can be challenging to find the right combination of strategies and tools that work for you.

If you’re new to budgeting or if you don’t feel confident with your current mix of budgeting tools, give proportional budgeting a try. A proportional budget divides your income into categories by percentage. It’s a simple concept to apply, it pairs well with the spreadsheets and/or apps you may already be using, and it can be easily tailored to suit your specific needs. Most importantly, it will make you think about your expenses in a completely new light.

In this guide, we’ll be using the 50/30/20 budget as a starting point. It was first introduced in a book written by Elizabeth Warren and Amelia Warren Tyagi, but has since been widely adopted as an effective intro to budgeting.

Step 1: Determine your limits

The 50/30/20 budget recommends that you spend 50% of your income on needs, 30% on wants and 20% on savings. Your first step is to calculate how much money those percentages represent for your particular financial situation. Take your monthly net income (that’s your take-home pay after taxes and deductions) and multiply it by 50%, 30% and 20% to determine your spending limits.

For example, if your net income is $3,000 a month, you would aim to spend $1,500 a month on needs, $900 a month on wants and $600 a month on savings.

Step 2: Track your spending

In order to measure your budgeting progress, you need to know where you’re at right now. Track your spending for at least two months. Capture your transactions however you like, but keep in mind that the more accurate you are, the more effective your 50/30/20 budget will be.

- Have your bank account and credit card statements handy to easily reference your purchase history

- Find a way to document cash transactions that aren’t captured electronically—a scrap of paper in your wallet or a note on your phone will do the trick

- Make sure your annual expenses are represented—list as many of your yearly expenses as you can (examples include annual subscription renewals, annual service and membership fees, and expenses like parking permits and property taxes) and divide them by 12 to calculate how much they cost you every month

Step 3: Sort your expenses

Once you have a snapshot of your monthly spending, sort each of your expenses from the previous month into one of three categories: Needs, Wants and Savings.

Needs are your absolute essentials. Skipping these expenses can lead to extreme hardship, job loss, illness or legal trouble. Therefore, your rent, your health insurance, your taxes and your credit card minimum payments fall under the needs umbrella.

Wants are all your non-essential purchases. Some of these non-essentials—like movie tickets, fast food and subscription services—are easy to identify. Others are trickier to spot because they can ride the line between needs and wants. For example, your typical grocery bill can include food staples like eggs, flour and veggies (need), snack foods or premium brands you prefer (want), household items like toilet paper and toothpaste (need) and personal care items like a fancy new shampoo (want).

By using 50/30/20, you’ll quickly realize that many of your needs are actually wants in disguise. Your basic rent is definitely a need, but if you’ve chosen to pay more for a gorgeous apartment in a prime location, then some of that payment should be coming out of your wants category.

- Split any bills that don’t fit neatly into one category. For example, let’s say your phone bill is $80 a month, and that includes your data plan and the smartphone that came with it when you signed up. Having a cellphone is probably a need, but your data plan and fancy phone are not—so consider $40 of it a need and the other $40 a want.

Savings are any expenses that go toward debt repayment (beyond minimum payments) or savings goals. Student loan payments, retirement savings and emergency fund savings all fit into this category.

- Keep in mind that saving money is not just for giant long-term goals like saving for a car or a home—short-term goals like a weekend trip or a computer upgrade can also fall under the savings umbrella

Step 4: Compare your percentages to 50/30/20

Add up your spending totals in each category and calculate what percentage of your income they represent. If your totals for needs, wants and savings already align to 50%, 30% and 20% respectively, then congratulations—you must be magical! Realistically, your totals will be different and that’s OK, because this will indicate where you need to make adjustments.

Step 5: Make adjustments

Every month, try to get closer and closer to the 50/30/20 limits you determined in Step 1. If you find you’re consistently overspending in a certain category, you have a few options available to you:

- Find cheaper options for regular expenses—see if there are expenses in your budget that you could reduce by switching service providers or going from brand name to generic

- Sacrifice something from another category—this is easier to do when you understand exactly how it affects your financial goals; packing a lunch instead of dining out feels more doable when you know that it will ultimately result in more spending money for your vacation next summer

- Increase your income—if you’re unwilling or unable to compromise on your spending, then you need to look for ways to make some extra money in order to maintain the 50/30/20 budget

After a few months, the 50/30/20 budget will feel natural to you: you’ll know which purchases are in line with your budget and which ones are not. You’ll have a better understanding of—and therefore more control over—your spending, and as a bonus, you’ll begin to notice that you’re closer to your savings goals than ever before.

Step 6: Keep at it

Some months are easier to budget than others. Don’t get discouraged if an unexpected expense or a moment of weakness throws you off your budgeting game. Keep tracking your spending and chasing that balance of 50/30/20.

- The 50/30/20 budget is a good starting point for many people, but it’s not set in stone. If 50/30/20 isn’t meeting your specific needs, try tweaking the percentages to better match your financial goals. A 30/10/60 budget skimps on wants, but will help you pay off a debt quickly. A 60/20/20 might be more suitable if you live in a city with high housing costs.

Proportional budgets like 50/30/20 help you determine what your priorities are and ensure that you’re spending your money in a way that’s aligned with those priorities. Whether you stick with it or ultimately transition to another system, 50/30/20 will shape your understanding of and confidence with budgeting.

Loading...

Loading...

Downloads

-

Loading...

-

Loading...

-

Loading...

-

Loading...